Strategic partnerships in the insurance sector are key to driving innovation, expanding market reach and increasing profitability. Many legacy providers seek partnerships specifically to modernize outdated legacy digital platforms and enhance customer experience.

However, these collaborations can also unlock a wealth of new opportunities for both insurers and their collaborators to expand reach, diversify and grow income sources and amplify customer engagement.

Below we explore various partnership models shaping success in the marketplace today.

6 models driving growth & innovation.

Lead-Sharing & Referral

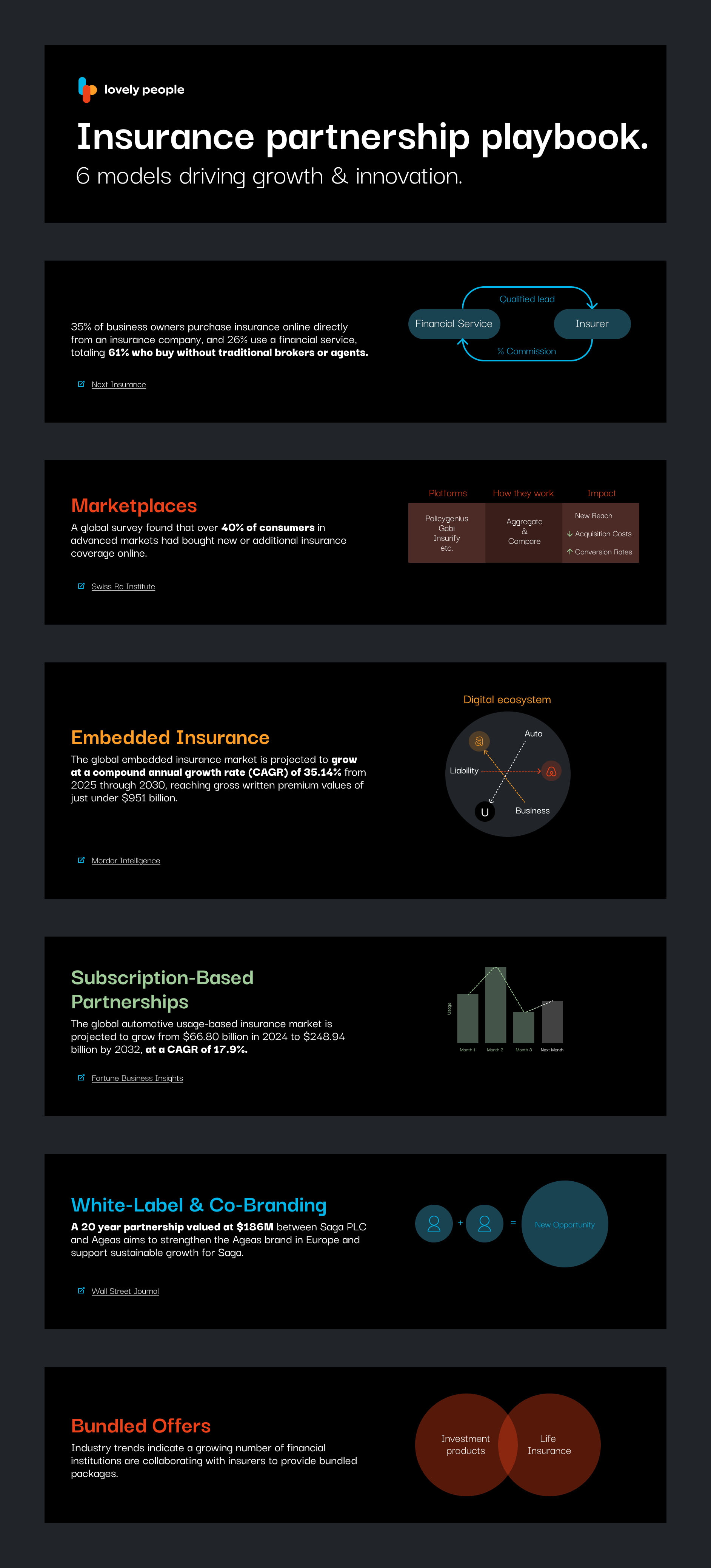

35% of business owners purchase insurance online directly from an insurance company, and 26% use a financial service, totaling 61% who buy without traditional brokers or agents.

Next Insurance

Marketplaces

A global survey found that over 40% of consumers in advanced markets had bought new or additional insurance coverage online.

Swiss RE Institute

Embedded Insurance

The global embedded insurance market is projected to grow at a compound annual growth rate (CAGR) of 35.14% from 2025 through 2030, reaching gross written premium values of just under $951 billion.

Mordor Intelligence

Subscription-Based Partnerships

The global automotive usage-based insurance market is projected to grow from $66.80 billion in 2024 to $248.94 billion by 2032, at a CAGR of 17.9%.

Fortune Business Insights

White-Label & Co-Branding

A 20 year partnership valued at $186M between Saga PLC and Ageas aims to strengthen the Ageas brand in Europe and support sustainable growth for Saga.

Wall Street Journal

Bundled Offers

Industry trends indicate a growing number of financial institutions are collaborating with insurers to provide bundled packages.

{kind=link}

In this model, fintech companies, financial service providers or other businesses refer clients to insurers, earning commissions for every successful policy sale. This approach is mutually beneficial — insurers gain access to new customer segments without significant marketing expenditures, while the referring partner secures a steady revenue stream through referral fees.

For example, financial advisory firms often partner with insurance companies to offer policies tailored to their clients’ needs, generating additional income through commission-based referrals. Digital aggregators and comparison websites also follow this model, connecting consumers with insurance providers while earning a percentage of the sale.

In this model, new or existing digital platforms act as insurance marketplaces and provide a centralized location where customers can compare and purchase policies from multiple providers. These platforms generate revenue in several ways, including listing fees paid by insurers for placement, commissions on each sale and subscription models for premium visibility.

By leveraging this model, legacy insurers benefit from increased exposure to potential clients, while marketplace operators capitalize on transaction-based earnings. Companies like Policygenius and Gabi have successfully implemented this approach, offering seamless digital experiences that allow customers to explore and purchase policies from multiple providers.

Embedded insurance is a growing model where non-insurance companies integrate insurance offerings into their primary products or services, eliminating transactional friction and enhancing customer value while generating additional revenue. This model is commonly used in sectors like travel, e-commerce, automotive and real estate and continues to grow by leaps and bounds. Mordor Intelligence reports recently projected the global embedded insurance market to grow at a CAGR of 35.14% — from 2025 through 2030 — with gross written premium values of just under $951B, with North America predicted to be the fastest growing market.

A few examples of embedded insurance collaborations are here —

- Amazon has partnered with Next Insurance to offer small business insurance policies directly through its online marketplace. This integration allows business owners to seamlessly purchase coverage tailored to their needs without leaving the Amazon platform.

- Tesla includes auto insurance options directly in its vehicle purchase process, providing customers with a seamless, hassle-free experience.

- Ride-sharing companies like Uber and Lyft partner with insurers to embed coverage for drivers, ensuring continuous protection without requiring them to purchase separate policies.

Embedded insurance not only increases convenience for customers but also allows insurers to scale their offerings without significant direct marketing efforts. The integrating partner, in turn, benefits from an added revenue stream and a stronger, value-driven relationship with its customers.

Some insurers are adopting subscription-based models in collaboration with digital platforms and service providers. In this arrangement, customers pay a recurring fee for coverage that can be adjusted or canceled as needed. This model is particularly popular in on-demand and gig economy industries, where flexible coverage is essential.

For instance, insurtech companies like Lemonade and Metromile use AI-driven subscription plans, offering pay-per-use and flexible policies. By partnering with other businesses, these insurers can provide tailored coverage, such as short-term rental insurance for Airbnb hosts or freelance health insurance for project-based workers.

Some insurers collaborate with partners to offer co-branded or white-label insurance products, where policies are marketed under the partner’s brand but underwritten by the insurer. Revenue is shared based on a pre-agreed structure, with the partner earning a percentage of premiums or profits from claims performance.

Retailers, financial institutions and e-commerce platforms often leverage this model to offer insurance directly to their customer base. For example, Amazon has partnered with insurers in select markets to provide product protection plans under its brand, enhancing customer trust while generating revenue through policy sales.

A common partnership model involves bundling insurance with complementary products or services, creating a seamless value proposition for customers. This approach enhances convenience and provides comprehensive solutions that meet multiple customer needs in a single package.

For example, financial institutions often collaborate with insurers to offer bundled packages, such as life insurance combined with investment products or homeowners insurance paired with mortgage services. This cross-selling approach benefits all parties — customers receive a streamlined solution, insurers gain access to a new customer base and the partners strengthen their respective service offerings.

Here’s an example. Lincoln Financial is collaborating with Bain Capital and Partners Group to launch private-market funds targeted at individual investors. These funds are offered through Lincoln's extensive network of financial advisers, allowing the company to effectively bundle diversified investment options to policyholders, generating a new revenue stream.

The rise of strategic partnerships in the insurance industry is transforming the way products and service offers are developed and delivered. From embedded arrangements and bundled offers to leveraging marketplaces, these kinds of collaborations are helping insurers stay competitive, enhancing customer engagement and creating new revenue opportunities.

By embracing innovation, insurers and their partners can adapt to evolving consumer needs to drive growth and create a competitive edge. Ready to explore your opportunities? Lovely People can help. Let’s talk.